Client Profile

Privately-Owned Foundry

140+ Years in Business

Avg Employee Count: 150

VERIS Outcomes

Total year one savings = $52,200

Total estimated year two savings = $646,200

Employer estimated surplus after 4 years = $1.3M

VERIS Proposed:

- 10% aggregate corridor

- Pay at Max model

- Annual rate caps on stop loss and total funding

Fully Insured:

- 2021 pricing based on actual renewal

- 2022 – 2025 Gross claims fund priced at 84% LR

- 2022 – 2025 Assumed med/rx trend at 10%

$1.5M | 2020 FI Premium

15.5% | January 2021 FI Renewal

$1.7M | 2021 FI Premium

Fully insured carriers may offer a rate hold as a good deal because it’s less than trend, but without access to claims data, employers don’t realize their claims suggest a rate reduction, not just a flat renewal.

The client saves 27% in healthcare costs by choosing VERIS vs. Fully Insured.

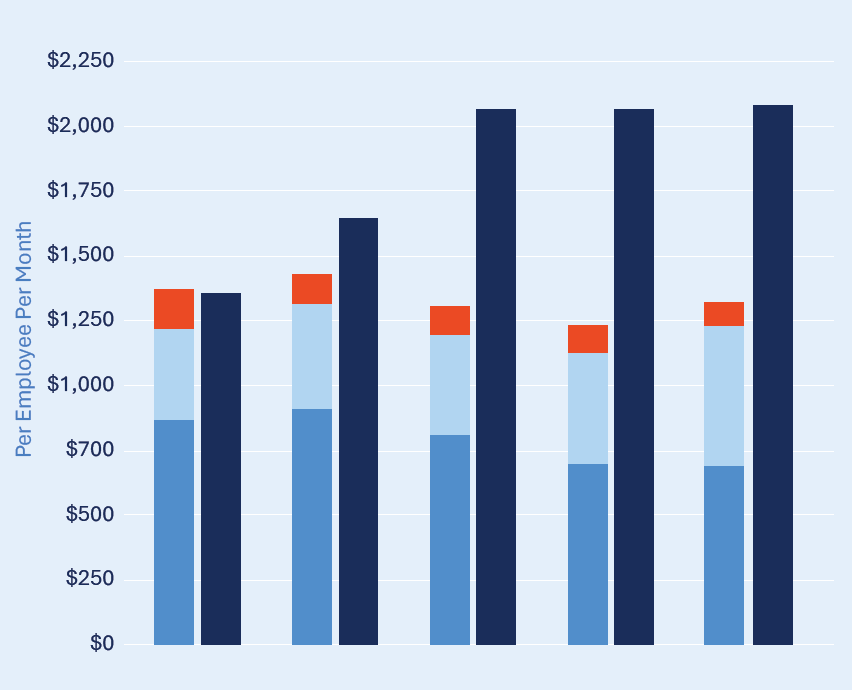

| 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|

| VERIS Admin | $97 | $70 | $70 | $67 | $59 |

| VERIS Premium | $327 | $353 | $361 | $409 | $480 |

| VERIS Actual Claims | $883 | $920 | $834 | $741 | $736 |

| VERIS Total | $1,307 | $1,343 | $1,265 | $1,217 | $1,275 |

| FI Total | $1,336 | $1,702 | $2,137 | $2,137 | $2,137 |

| VERIS PEPM SAVINGS | $29 | $359 | $872 | $920 | $862 |